Finance for Beginners: Basics Of Savings

9 mins read

Posted by Mobolaji Ajanaku

Published on Jul 25, 2024

Introduction

Imagine your financial future as a house. Would you like to build that without a strong foundation? Definitely not. Think of that concrete base you need as your savings. Think of it: whether you're looking forward to a beach vacation, changing houses, or you just want to be ready for life's unpredictability, having savings will help.

Better still, you do not need to be a financial genius or earn a fortune to be able to do this. By taking the right steps, everyone can create a stable financial future. With this guide, we aim to break down the basics of saving money into an easily understandable. Let's get going!

What Is Saving or Savings?

Let's start with the very basics. Saving is simply setting aside some of your income for yourself rather than consuming all of it. Imagine it like you're giving yourself a future gift and also knowing you have some money to fall back on if the need arises, whether it be for emergencies, big purchases, or, you know, just to feel safe. Saving is kind of like planting a tree: the sooner you plant it, the more time it has to grow.

In financial terms, savings refer to the portion of your income that you do not spend on current expenditures. Instead, you store this money in various accounts or investments, where it can grow or be used for future needs.

In layman's language:

Saving is the act of setting aside money for the future.

Savings is the money that has been accumulated from those actions.

Why Should You Save?

So why, you're probably wondering, should you save? The first and most obvious reason is that savings contribute to your financial safety. There are always those sharp and unexpected turns in life, and having savings stashed up somewhere can cushion you from such eventualities. It could be having to pay an unplanned medical bill or a car fix without needing to borrow extra money. Second, saving helps you achieve your goals. Be it for your dream vacation, a new house, or starting a business. To make these dreams a reality, you could save for them.

Also, saving isn't just for emergencies or big purchases; it's also to prepare for things like education, retirement or even that bag or device you like. Consider it similar to preparing for a rainy day so that you are not caught by surprise when one actually hits.

Who Should Save?

Here is the catch: saving is for all, young and old, low- or high-income earners. It is not a preserve for high-income earners or for those nearing retirement. Even if you're just starting to earn money, cultivating a savings culture will pay off later. Of course, the specific needs for saving differ among specific groups—beginners, young professionals, and those nearing retirement. Yet the principle remains the same.

When to Start Saving

When should you begin saving? Early. The earlier, the better. Because with compound interest (more on that later), even the small amounts you save regularly will miraculously amount to significant figures in the future. Interest earns interest, and you keep snowballing the savings. But what if you haven't started yet? Don’t worry. You can never be too late to start a habit of saving. The most important thing is to start today. It is always better to start as early as possible and give yourself a head start. The key is to make it a regular part of your financial routine. So, regardless of whether you are 18 or 60, you can reap the benefits.

Where Should You Save?

Now, let's talk about where to stash your cash. As simple as it sounds, a good, old-fashioned savings account is a great place to start. They’re easy to open, plus your money will be safe and within reach. Look for zero-fee accounts with good interest rates to make the most of your savings. If you're ready to bring your A-game, enter the high-interest savings account. That usually translates to higher interest rates, so the money grows in value faster. They may require a higher minimum balance, but, hey, that extra interest can add up.

Certificates of Deposit (CDs) are another option if you can set aside money for a fixed term. CDs offer higher interest, but your cash has to be stashed for a minimum length of time, ranging from a few months to years. It's a great way to make more money off of interest if you don't need the money right now.

Money market accounts are yet another good option. A money market account combines the features of both a savings and checking account, typically with a better interest rate than what you would get on an ordinary savings account.

You may also want to consider the following:

- Retirement accounts, like IRAs and 401(k)s: These are tax-advantaged and perfect for long-term savings.

- Investment accounts are those through which stocks, bonds, or mutual funds can be purchased with higher return opportunities, but also at higher risks.

- Health savings accounts: If you're eligible, it allows you to save for medical expenses with tax benefits.

- Savings for education: 529 plans or other specifically education-oriented savings accounts.

Each has its advantages, depending on your financial goals and time horizon.

How Do You Start?

So you're convinced, but how do you actually start your saving journey? First things first, set your goals. What is it that you are saving for? Is it a house, a vacation, a car, or something as small as a bag? Make sure your goals are attainable and realistic so you can continue practising how to manage your spending effectively. And then build a budget. This doesn't even have to be complicated. Remember our article on budgeting? You just need to track your income and spending and take a look at where you could take it down a notch. Simple changes like making coffee at home, cancelling unused subscriptions, or doing more home-made meals will really add up over time. Every little bit helps.

Automating your savings is also a very good idea. You can have an automatic transfer set up where a small amount of your salary goes directly from your checking account to your savings account. That way, saving is no longer an afterthought. You won't even miss the money since it's out of sight, out of mind. Try to earn more through side hustles, freelancing, or selling things you don't need anymore. Earning more will bring in more money to save and, eventually, make any process exciting for trying new opportunities and skills.

Key Terms in Savings

Before we continue, let us highlight some very critical concepts and terminologies related to saving money.

Emergency Fund

One of the first goals for you to start saving should be building an emergency fund. Consider this fund as your financial backup, designed to cover unexpected expenses like medical bills, car repairs, and, we hope not, a sudden job loss. Try as best as you can to save enough to cover at least 3–6 months' worth of living costs. Having this backup will surely prevent you from going into debt when you face any hardship.

Compound Interest

For us, a compound interest rate feels like sprinkling a little fairy dust on your savings. For example, if you save $100 a month in an account that pays 5 percent per year, after one year, you will have deposited $1,200; with interest, you will have about $1,230. Interest earns interest, so the longer it goes, the faster your savings will grow. Start early and let time do the heavy lifting for you.

Principal

It simply refers to the actual amount of money one deposits into savings or any investment. For example, depositing $500 in a savings bank means $500 in principal. It is important because the interest will be based on this amount.

Interest Rate

This is the percentage by which your money grows over time in your savings account. For example, if you have an account with a 2% interest rate, every year your money will grow by 2%. The higher the interest rate, the faster your savings will grow.

Inflation

Inflation reflects the rate at which levels of general prices of goods and services are increasing; it therefore lowers the purchasing power of money. In saving, it's important to select accounts with interest rates that at least match inflation to ensure your money maintains its value over time.

More Helpful Tips For You

If you're the type of person who has a hard time sticking with a savings plan, figure out how you might be able to save with an element of fun and participation. Make use of graphic aids for tracking your progress or work with a savings challenge. Try the 52-week savings challenge, where you save $1 the first week, $2 the second week, and so on until you save $52 in the last week. By the end of the year, you’ll have saved $1,378! There’s also the $5 savings challenge—every time you get a $5 bill, just set it aside. It can be really satisfying to see how much you have achieved, and it keeps you on track.

Thankfully, in this digital era, there are numerous apps that can make saving easy work for you. Check out these tools or applications to find what works best for you. Also, keep learning about personal finance. Many good resources, from books and blogs to online courses, are at your disposal. The more you know, the better you save. Besides, in a case where it is really necessary, seek advice. When you doubt your savings plan or need personalized guidance, a financial advisor may be of full help. They can help you design a plan that works best for your specific case.

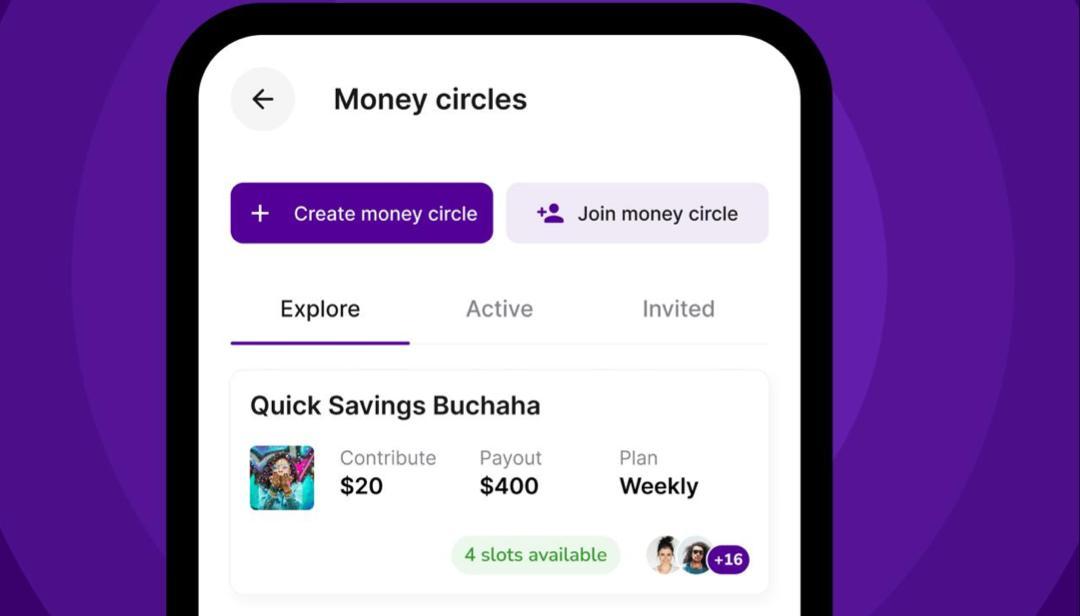

Not to mention, the money circles feature on the Plently app. These circles are created to provide support and keep you motivated and accountable during your saving journey.

Conclusion

Getting started on your savings doesn't have to be a difficult process. We have outlined here basically everything that you must know in order to be successful at it. Start small and keep doing it—you'll find your savings blooming. And there you go, folks—just a basic beginner's guide to get you on board on this journey. Remember, the most important thing is to just get started. Good luck!

Last updated: Jan 14, 2025

Share this with your friends and family

Join the money party

Level up your financial game with our exclusive blog updates, delivered straight to your inbox

Other articles you might enjoy

Join the #1 banking app for the Commonwealth

Get started on Plently

Rosemary D.

Phia Consultants

It's like having the best financial partner in my pocket!

Jonathan G.

Open Space Inc

Plently has truly transformed my financial life.

Emily H.

Student

With their user-friendly interface and innovative tools, managing my money has become a breeze.

Margaret D.

Small Business Owner

I finally feel in control of my finances, thanks to Plently!

Alexander P.

Small Business Owner

After Plently, I can't imagine going back to traditional banking!

Oliver A.

Student

Being a part of a Money Circle has been a game-changer for me. It's not just about financial contributions; it's a supportive community working together towards shared goals

Loading comments...